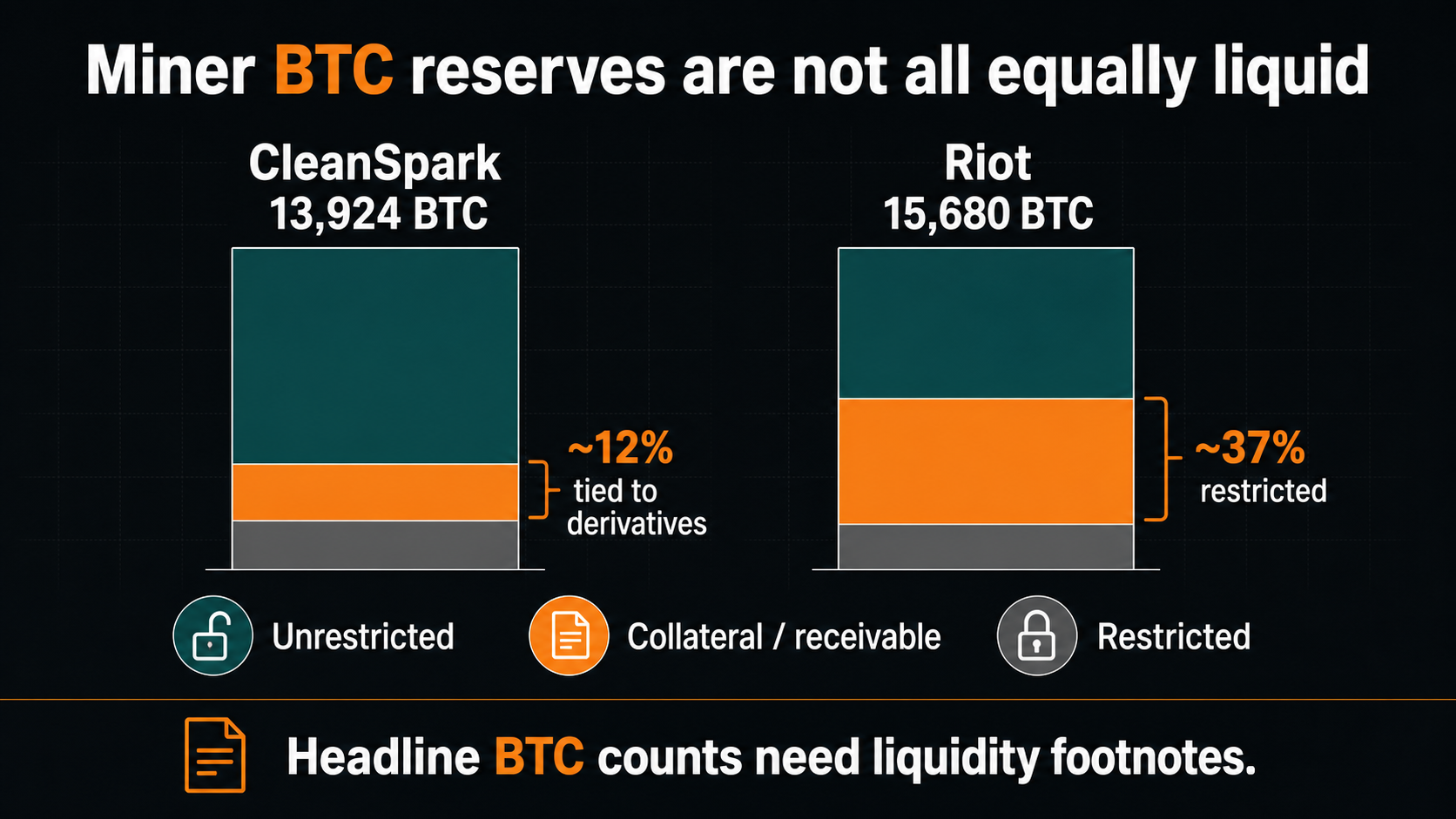

Bitcoin miners are using up to 12% of treasury BTC as collateral rather than selling coins

Top public Bitcoin miner CleanSpark’s latest BTC count carried a footnote that may matter more than the headline total: of the 13,924 BTC it reported as of June 30, 1,719 BTC was posted as collateral or recorded as a receivable, all tied to derivative transactions

That amounts to roughly 12% of the miner’s reported Bitcoin balance held in financing or risk-management mechanisms rather than functioning as a readily available reserve.

For reference, CleanSpark currently owns the 11th-largest public Bitcoin treasury among operating companies.

The disclosure does not imply misuse. It does show why miner treasuries are getting harder to read as the same BTC stacks are marketed as strength, sold for cash, pledged, restricted, or moved through derivatives.

The reserve count is no longer one number

CleanSpark still produced 614 BTC in June, but its treasury line moved through more than production. The company said it sold 179 BTC at spot, sold 250 BTC pursuant to call exercises, acquired 25 BTC pursuant to put exercises, and acquired 244 BTC related to a delta-neutral basis trade.

Riot Platforms provides the market with a broader comparison point. In its Q1 2026 operations update, Riot reported 15,680 BTC held at quarter-end, including 5,802 restricted BTC, after selling 3,778 BTC for $289.5 million in net proceeds. That restricted balance equaled roughly 37% of Riot’s reported holdings.

The comparison is not about whether collateralized or restricted BTC is bad. It is about liquidity. A miner with 15,000 BTC on the headline line may not have the same stress buffer as another miner with the same headline balance if one reserve is mostly unrestricted and the other is partly pledged, restricted, receivable, or linked to derivatives.

That difference can change how the market interprets the same balance sheet number. A company can still hold a large BTC stack while part of that stack is already serving a financing, collateral, or settlement role. In weak markets, those footnotes move from accounting detail to liquidity signal.

The timing makes those footnotes even more important.

CryptoSlate’s Bitcoin page showed BTC near $62,000 on July 8, about 50% below its October 2025 all-time high.

CoinShares’ Q1 2026 mining report said listed miners’ weighted-average cash cost to produce one BTC had risen to about $79,995 in Q4 2025, while hashprice near $30 per PH/day left an estimated 15% to 20% of the global fleet underwater amid higher power costs.

CoinShares also said listed miners could derive as much as 70% of revenue from AI by the end of 2026, up from roughly 30%, after more than $70 billion of announced GPU colocation and cloud service deals with hyperscalers.

That shifts the question from who has the most BTC to who has deployable BTC when capital needs rise. That is the new balance-sheet question for miners.

The stress test is liquidity

If BTC and hashprice stay weak, the first thing to break may not be the network or even the headline reserve. It may be the assumption that every reported coin can be used quickly to fund power bills, debt service, AI and high-performance computing buildouts, or working capital, without creating a new constraint elsewhere.

The next June and Q2 miner updates should show whether CleanSpark’s disclosure is an outlier or a preview. Investors will be watching not just how many BTC miners hold, but how many are unrestricted, how many are collateral, how many are receivables, and how many have already been monetized before the market counts them as dry powder.

The post Bitcoin miners are using up to 12% of treasury BTC as collateral rather than selling coins appeared first on CryptoSlate.